About thirty years ago, the advent of the Internet changed the growth trajectory of American businesses. Since then, many new technologies, innovations and high-profile trends have emerged, promising to be the best thing since sliced bread. However, none have come close to matching the potential for change brought by connecting the world via the Internet…until now.

The arrival of artificial intelligence (AI) opens unlimited doors in virtually every sector and industry. When I say “AI,” I’m referring to the use of software and systems for tasks that would normally be overseen or undertaken by humans. Giving software and systems the ability to learn and evolve over time without human intervention is what makes AI so useful.

According to a report released last year by PwC analysts, AI could add around $15.7 trillion to the global economy by the end of the decade. That’s a huge amount of money and a pie big enough to allow for multiple winners.

But so far, no company has been a bigger winner in AI than the semiconductor company. Nvidia (NASDAQ:NVDA).

Nvidia leveraged its competitive advantages to a much-needed stock split

In a short time, Nvidia’s graphics processing units (GPUs) have become the standard in compute-intensive data centers. According to a study by semiconductor analytics firm TechInsights, Nvidia was responsible for shipping 3.76 million of the 3.85 million GPUs destined for AI-accelerated data centers in 2023. This represents a market share of 98% and effectively borders on a monopoly.

There’s no doubt that AI-focused companies want Nvidia GPUs in their data centers to help them train extended language models (LLMs) and oversee generative AI solutions. This is quite evident when you consider that approximately 40% of Nvidia’s net sales come from members of the “Magnificent Seven.” Microsoft, Metaplatforms, AmazonAnd Alphabet. During Meta’s first quarter, the company announced plans to increase its capital spending, with the express idea of providing a springboard for its AI ambitions.

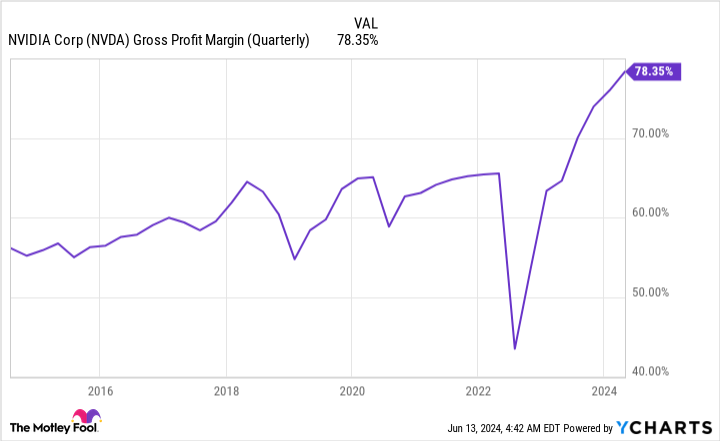

The first-mover advantage has also fueled Nvidia’s pricing power. Demand for the company’s H100 GPU has completely outpaced its ability to fill orders. Even with Semiconductor manufacturing in Taiwan By strengthening its chip-on-wafer-on-substrate capacity, Nvidia is unable to satisfy all of its customers. As a result, he was able dramatically increase the selling price of its GPUs, which led to a scorching 78.4% gross margin in the fiscal first quarter (ended April 28).

Nvidia’s advantages in AI-accelerated data centers, coupled with the mountain of cash flow generated by its high-priced H100 GPUs, also help support continued innovation. In March, the company unveiled its Blackwell GPU architecture, designed to further accelerate computing capacity in the areas of data processing, quantum computing and generative AI.

Earlier this month, CEO Jensen Huang revealed Nvidia’s new AI architecture, codenamed “Rubin.” Rubin will help train the LLMs and operate on a new central processor known as “Vera.” While Blackwell is expected to arrive in customer hands later this year, Rubin won’t officially debut on a commercial scale until 2026.

This combination of innovation, first-mover advantages, and supernatural pricing power has driven Nvidia’s stock price up more than 700% since the start of 2023. As the company’s shares have recently exceeded well over $1,000 per share, its board approved and executed a 10-for-1 stock split. Nvidia joined more than a half-dozen other high-flying companies in carrying out a stock split in 2024.

On paper, we couldn’t dream of a more perfect sales ramp-up than that proposed by Nvidia. But when things seem too good to be true on Wall Street, they almost always are.

Even if Nvidia maintains its computing advantages, shareholders can still lose

As an investor, you should look for companies that have well-defined competitive advantages, or even impenetrable moats. At the very least, Nvidia accounting for 98% of AI GPUs shipped in 2023 puts it in the top category.

But even if Nvidia maintains its competitive advantages in GPUs, it may not be enough to keep its stock from collapsing.

For example, it’s well documented that Nvidia is about to face its first real bout of external competition, including Intel (NASDAQ:INTC) And Advanced microsystems (NASDAQ:AMD). Intel’s Gaudi 3 chip, which accelerates AI, will be widely available to customers in the third quarter. Intel says Gaudi 3 has advantages in inference and power efficiency over Nvidia’s H100.

Meanwhile, AMD is ramping up production of its MI300X AI-GPU, designed as a direct competitor to Nvidia’s wildly popular H100. The MI300X outperforms the Nvidia H100 in memory-intensive tasks, such as simulations.

Even if Blackwell and Rubin end up blowing Intel and AMD’s chips out of the proverbial water based on compute capacity, the scarcity of GPUs suggests that Intel and AMD may still be big winners. A significant delay in Nvidia chips should roll out the red carpet for external competitors like Intel and AMD.

And it’s not just external competitors that pose a potential problem for Nvidia. The company’s aforementioned major customers, which account for about 40% of its sales, all develop AI GPUs for their data centers in-house. This includes Microsoft’s Azure Maia 100 chip, Alphabet’s Trillium chip, Amazon’s Trainium2 chip, and the Meta Training and Inference Accelerator (MTIA) of the giant social media meta platforms.

Are these AI chips currently a threat to Nvidia’s computing advantage? No, but their mere presence as a complement to the H100 GPU removes valuable data center “real estate” and signals that Nvidia’s core customers are deliberately reducing their reliance on the AI pivot.

With more AI GPUs available from Intel and AMD, and many AI chips developed in-house by Magnificent Seven, the GPU shortage that has propelled Nvidia’s pricing power into the stratosphere will diminish. The company’s adjusted gross margin guidance of 75.5% (+/- 50 basis points) for the fiscal second quarter – a decline of 235 to 335 basis points from the sequential quarter – likely indicates that these pressures settle down.

Additionally, every high-profile technology, innovation, or trend over the past three decades has succumbed to an early bubble burst event. Investors have consistently overestimated how quickly a new technology, innovation or trend would be adopted by businesses and/or consumers.

Although AI resembles the second coming of the Internet in terms of changing the growth arc of American businesses, most companies do not have a well-defined game plan for how they will deploy AI. technology to improve their sales and profits. We see this overzealousness repeated cycle after cycle with the largest investments.

Please note, this does not mean that Nvidia will not be very successful in the long term or that its shares cannot still increase in value in 10 or 20 years. But it suggests that while Nvidia maintains its competitive edge in GPUs, the technology’s immaturity in its early days has primed Wall Street for another bubble.

The leader of all major innovations for three decades finally saw its share price fall by at least 50%. I think Nvidia shareholders are about to experience the same disappointment.

Should you invest $1,000 in Nvidia right now?

Before buying Nvidia stock, consider this:

THE Motley Fool Stock Advisor The analyst team has just identified what they think is the 10 best stocks for investors to buy now…and Nvidia wasn’t one of them. The 10 selected stocks could produce monster returns in the years to come.

Consider when Nvidia made this list on April 15, 2005…if you had invested $1,000 at the time of our recommendation, you would have $794,196!*

Equity Advisor provides investors with an easy-to-follow plan for success, including portfolio building advice, regular analyst updates, and two new stock picks each month. THE Equity Advisor the service has more than quadrupled the return of the S&P 500 since 2002*.

*Stock Advisor returns June 10, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, former director of market development and spokesperson for Facebook and sister of Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Sean Williams holds positions in Alphabet, Amazon, Intel and Meta Platforms. The Motley Fool holds positions and recommends Advanced Micro Devices, Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Intel and recommends the following options: long January 2025 $45 calls on Intel, long January 2026 $395 calls on Microsoft, short August 2024 $35 calls on Intel, and short $405 calls in January 2026 on Microsoft. The Motley Fool has a disclosure policy.

Even if the Nvidia stock split maintains its competitive advantages in GPUs, its shareholders could be in for a nasty surprise was originally published by The Motley Fool