")

baileystock

My thesis

The fact that Tesla’s (NASDAQ:TSLA) market capitalization is multiple times higher than its intrinsic value means that the stock and Elon Musk have a huge fan base believing in long-term growth potential.

My intrinsic value calculations suggest that Tesla’s fair stock price is about four times lower than the last close. The valuation looks especially unfair considering all the headwinds and fundamental problems Tesla faces. The Fed remains quite hawkish and is expected to remain so for longer, which is a big headwind for the company. Tesla’s 8.7% revenue decrease in Q1 was much worse compared to the performance of the global (18% growth) and U.S. EV markets (2.6% growth). This means that Tesla is losing market share and is struggling to deal with the intensifying competition. The competition is likely to intensify further, which is another bad sign for Tesla. Even Tesla’s discounts for its models do not help in driving revenue growth, while profitability profile suffers a lot.

This collection of catalysts looks very bearish, and significant overvaluation means that TSLA is a Strong Sell for me.

TSLA stock analysis

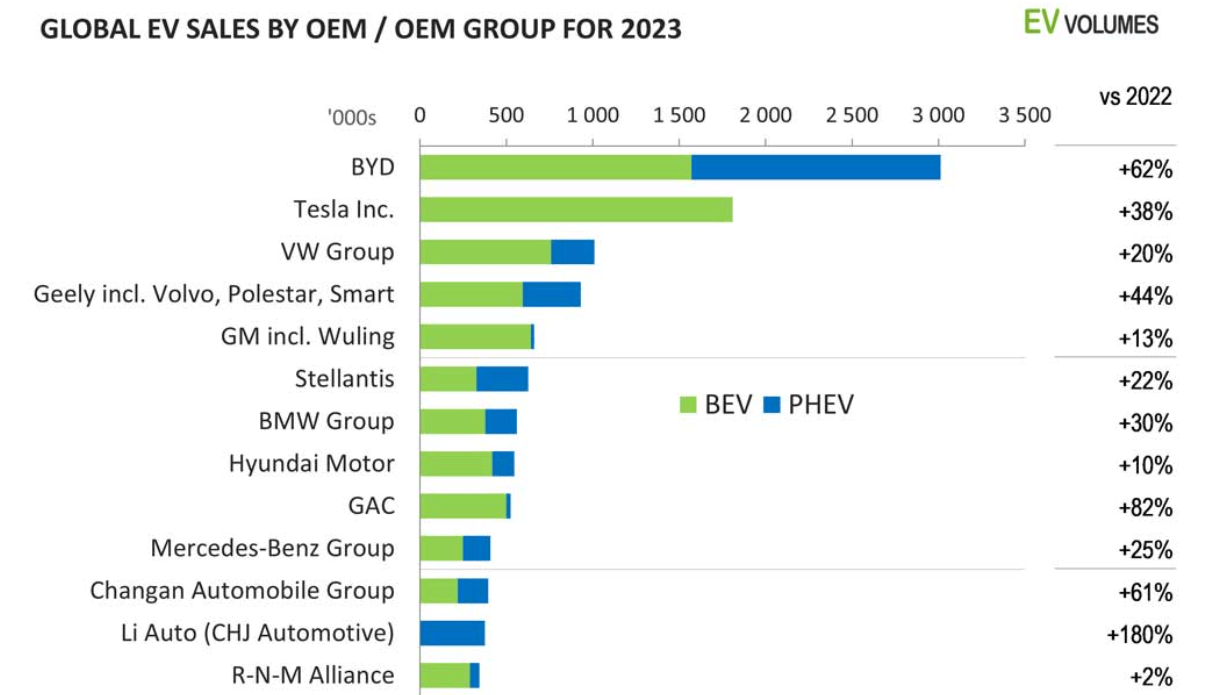

Tesla is the world’s largest automotive company by market capitalization. However, Tesla is not the largest manufacturer in terms of volumes with around 2 million cars per year, five times less compared to Toyota’s (TM) 10 million units annually. Tesla’s market cap is currently above $630 billion, more than twice as high as Toyota’s (TM). I will speak about valuation in detail in the next part of my analysis, but such an inconsistency at high-level looks unfair. Tesla is surely the number one battery EV manufacturer in the world, but I prefer not to separate EVs from internal combustion engine (ICE) cars when we compare automotive companies volumes. I am not separating because Tesla’s cars compete for customers’ money not only with EVs but with ICE vehicles as well.

ev-volumes.com

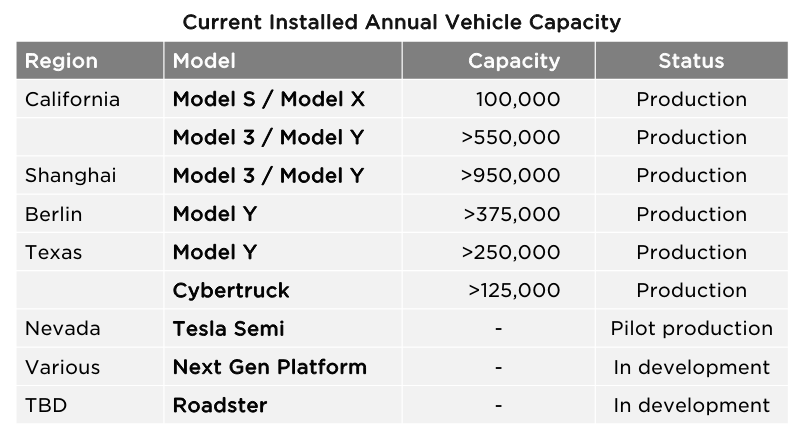

Tesla’s capitalization was soaring during the pandemic, especially after Elon Musk announced an extremely bold goal of achieving 20 million cars sold per year by 2030. With only five more full years ahead and the current 2 million deliveries per year, achieving this bold goal is unrealistic, in my opinion. Growing deliveries number by 10 times over five years means a 58.5% CAGR, which is very unlikely. Moreover, to produce 20 million cars per year, Tesla’s production capacity shall expand by four times. Thus, achieving 20 million cars per year is certainly unrealistic.

Q1 Investor Deck

I consider the current environment of high-interest rates to be the big constraint for Tesla’s ambitious plans, both from the demand and capacity sides. Elon Musk admitted that interest rates are working against the company’s financial success as they reduce the affordability of vehicles. As long as the Fed’s decision makers’ stance remains hawkish, we cannot expect a rebound in demand for any cars, not just EVs. Only one rate cut in 2024 looks like quite a hawkish approach, especially considering that at the beginning of this year, the Fed projected three rate cuts.

DT Invest

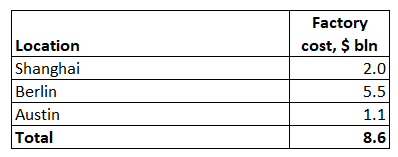

High-interest rates do not only badly influence the demand for Tesla’s cars, but also limit its ability to invest in expanding capacity. Figures vary from resource to resource, but my research of public sources suggests that the total cost of completing Tesla’s gigafactories in Shanghai, Berlin, and Austin was $8.6 billion. These factories’ total capacity is 1.7 million per year. Extrapolating this logic means that Tesla will need to invest around $38 billion more to achieve a 20 million capacity. Tesla’s balance sheet is strong, but even for the company’s financial position, $38 billion is a huge amount and the company will definitely need to raise debt. In a high-interest rate environment like we see now and will probably see through 2025, raising massive debt amounts is quite unlikely. Taking into account all that I have mentioned above, achieving even 10 million annual cars sales by 2030 is unrealistic.

And the current monetary environment is not the only secular headwind for Tesla because the competition is intensifying rapidly. It is certain that Tesla struggles to deal with intensifying competition when we compare the company’s 8.5% YoY revenue dip in Q1 to the 18% growth in global EV sales over the same period. Interest rates in the U.S. are high, but the domestic EV industry showed a 2.6% YoY growth in Q1. Tesla was significantly behind the EV market, likely meaning that its products are losing their appeal, especially recalling that Tesla was cutting prices across all models.

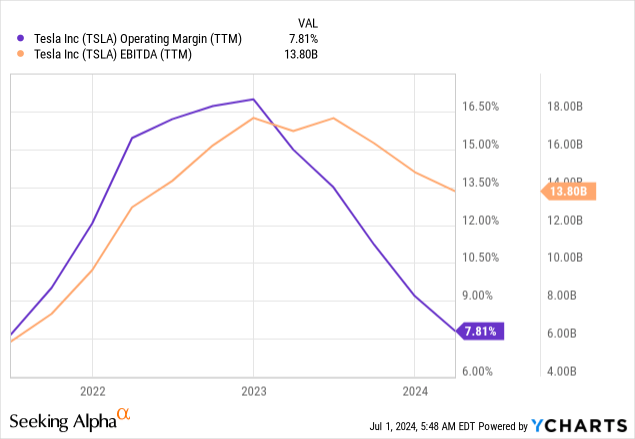

Tesla’s profitability was also one of the main arguments of the stock’s bulls. A 16-17% operating margin was really impressive, but it turned out to be unsustainable, and TSLA’s operating profitability right now does not look that impressive. Shrinking profitability together with revenue growth lagging compared to industry looks really bad.

The situation with revenue growth and profitability is unlikely to improve soon because the competition will continue intensifying. Toyota plans to roll out multiple EV models in 2026. Audi plans to spur electrification in the next two years as well. Volkswagen (OTCPK:VWAGY) will also add more competition with its recently announced partnerships. The German giant not only plans to develop five new EV models in partnership with Chinese SAIC Group, but will also invest $5 billion in Rivian Automotive (RIVN).

From the bulls’ side, I can say that Tesla invests a lot in R&D in order to innovate and differentiate. TTM R&D expenses are $4.3 billion, a large amount even for a company with a $631 billion market cap. There is no available breakdown, but I think that R&D expenses are mostly allocated to designing and developing new models. Tesla’s most fresh model releases were the fully electric commercial truck called Semi and the electric pickup called Cybertruck. The pickup looks interesting with its ultra-hard stainless-steel exoskeleton and armor glass. However, these models are too young and deliveries are insignificant at the moment, which makes it difficult to assess them. Moreover, sales are unlikely to soar at least until interest rates are high.

Intrinsic value calculation

Due to all the headwinds, Tesla’s current $631 billion market cap can likely only be explained by enormous growth expectations. In my discounted cash flow (DCF) model, I will try to be as fair as possible and incorporate reasonable growth assumptions. But before we speak about growth in revenue and profitability, I need to find out the discount rate.

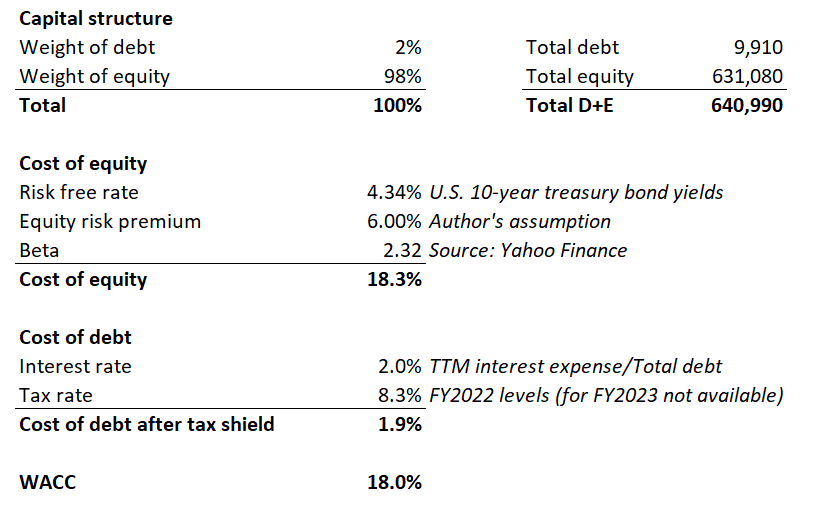

Based on the capital asset pricing model, Tesla’s weighted average cost of capital (WACC) is 18%. I will use this percentage as a discount rate. WACC calculations are outlined below, with all variables described.

DT Invest

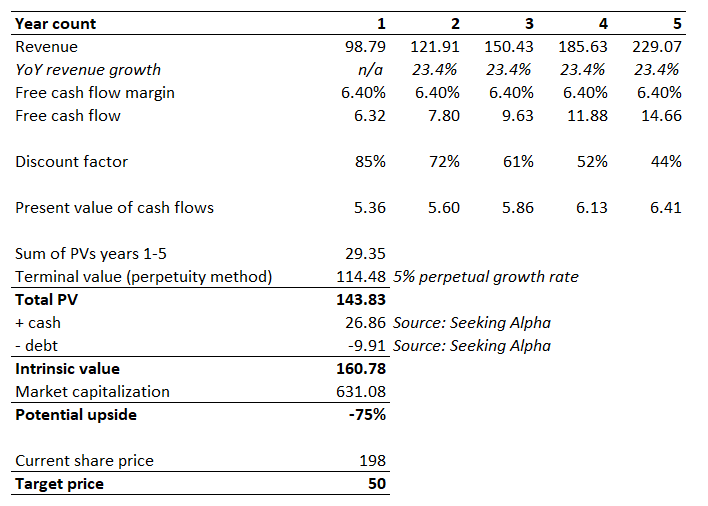

Year 1 $98.8 billion revenue assumption is from consensus estimates. According to Precedence Research, the global EV market is expected to compound with a 23.4% CAGR. I incorporate this as revenue CAGR for years 2-5. Tesla’s past five years’ average FCF margin is 6.4%. I use this level flat, because with the intensifying competition it will be extremely difficult for Tesla to drive free cash flow margin. Since EV is a thriving industry, I give Tesla an optimistic 5% perpetual growth rate.

DT Invest

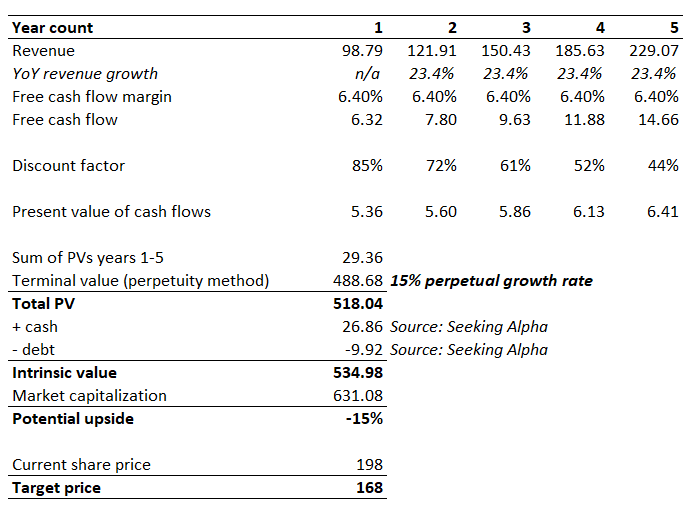

Tesla’s total intrinsic value, including net cash, is $161 billion. The potential downside is massive, which means that my target price is $50 per share. Terminal value represents the lion’s part of the total intrinsic value, meaning that the financial model is susceptible to changes in the perpetual growth rate. In Tesla’s case even implementing an unrealistic 15% perpetual growth rate does not make the stock’s valuation look good.

DT Invest

What can go wrong with my thesis?

Having such a premium over its intrinsic value means that lots of investors believe that Tesla deserves it. Bulls usually name various potential moonshots, which include the Full-Self Driving (FSD) feature for vehicles, energy storage business, and even the Optimus humanoid robot. The future of these projects looks quite uncertain, in my opinion. However, it is difficult to deny that Elon Musk is an extraordinary entrepreneur who has built several disruptive businesses in his life. I apparently do not have such a visionary talent as Elon Musk has, and I might be missing something in my bearish opinion. If the industry of humanoid robots becomes worth trillions, Tesla might benefit from it as one of the pioneers. Therefore, the level of uncertainty around new projects is high, but this uncertainty does not necessarily mean only negatives.

Elon Musk is not only a talented visionary, but he is also very talented in impressing investors with his presentations and earnings calls. Despite revenue decline in Q1 and profitability decreasing, the stock currently trades 38% more expensive than it did a week before the Q1 earnings release. The reason of this rally is Elon Musk’s talent of impressing investors with potential new projects like Robotaxi. While Elon Musk theoretically speaks about Robotaxi potential, Google’s (GOOGL) Waymo already operates in some of the large U.S. cities.

Summary

Tesla’s valuation is not deserved, even if revenue growth is assumed to be quite fast. The premium is unlikely to be reasonable, especially considering all the headwinds and fundamental issues I described in my analysis.