")

baileystock

Over the last couple of weeks, one of the stocks in the market that has done the best has been Tesla (NASDAQ:TSLA). The electric vehicle giant has seen shares rise significantly after some optimism built surrounding Q2 unit volumes, helping to put a very weak Q1 in the rearview mirror. Tuesday morning, Tesla published its quarterly production and delivery report, with all the numbers providing a nice surprise for the bulls.

My previous coverage:

It was back at the Q1 earnings report when I last covered Tesla. At that time, the company reported disappointing headline numbers, with a number of headwinds suppressing production and deliveries in the period. Management also detailed cash burn of more than $2.5 billion for the quarter, but yearly guidance wasn’t as bad as it could have been.

At that time, I upgraded the stock from a sell to a hold. Elon Musk revealed that Tesla would change its plans up a bit, focusing on some more affordable vehicles in the short to medium term rather than going all in on the so called “$25,000 EV” first. Since that time, Tesla shares have surged roughly 40%, compared to a high single digit percentage gain for the S&P 500.

Q1 figures come in very strong:

Over the last couple of months, Tesla volume estimates have been coming down thanks to that Q1 weakness. Some of that has been due to a slower than expected refresh of the Model 3 Performance variant in the US, while fears have grown over competition in China. European sales also have struggled at times, resulting in Tesla offering numerous discounts and promotions worldwide in Q2. In the end, these marketing efforts paid off, as the results below show:

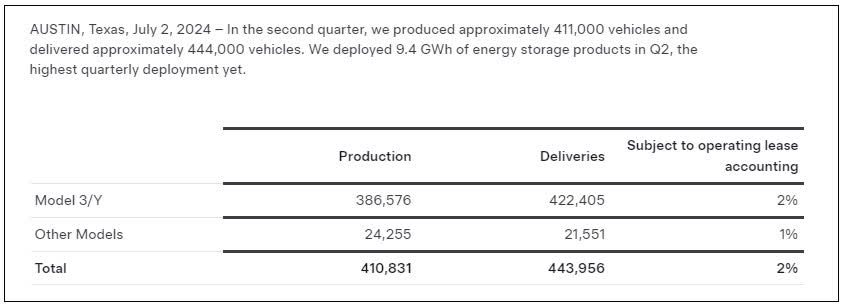

Tesla Q2 2024 Volumes (Company Press Release)

When Tesla sent out its investor relations compiled analyst estimate average, the street number for deliveries was under 438,000. That number itself seemed rather high, with most whisper numbers being in the 415k-425k area. We’ll have to wait a few weeks to see how certain countries did and if there were any fleet sales involved here, but all things considered, this was very solid. The only negative is that this was still a roughly 5% decline over the prior year period, despite the addition of the Cybertruck.

It will be very interesting to see how the low production numbers impact Tesla’s margins, as it appears factory shutdowns were much larger than originally expected. The good news is that a bunch of inventory was cleared here, which is good for cash flow. Additionally, energy storage deployments more than doubled from Q1 levels, well above what anyone was expecting, so that should help the company’s overall revenue number.

The next step in the process:

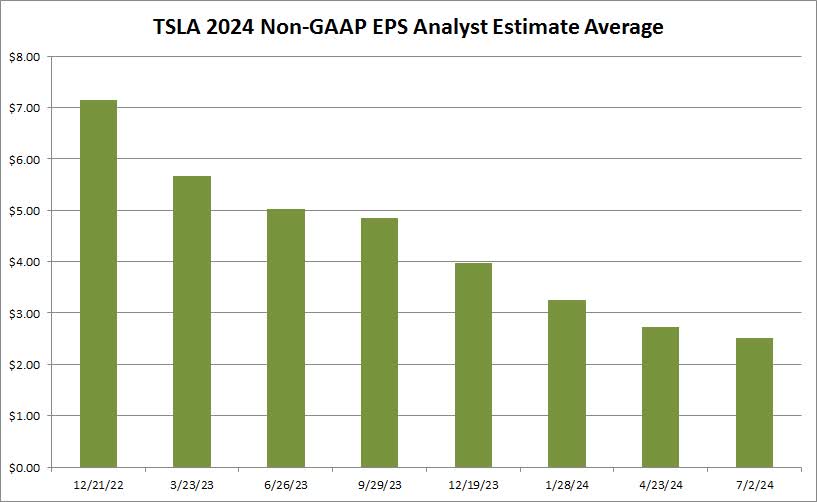

Perhaps the biggest item to watch in the short term will be analyst estimates. Revenue estimates should definitely rise a bit into the earnings report in three weeks. I think the street will start to be more positive on the adjusted bottom line as well, when excluding the likely large restructuring charge that Tesla will have taken in Q2 to improve its overall cost structure. As the chart below shows, adjusted earnings estimates for this year went into Tuesday’s report basically at their lowest point, but a reversal in that trend could be coming rather soon.

Tesla 2024 Expected Adjusted EPS (Seeking Alpha)

Tesla will report its full set of Q2 results on Tuesday, July 23rd, after the bell. While the numbers will be fun to break down as usual, the more important date is a few weeks after that on August 8th. The company will unveil its long awaited robo-taxi on that date, with some bulls also hoping to see a reveal of these new “more affordable” models coming or perhaps even a ride hailing service launched. With Elon Musk, Cathie Wood, and so many others calling for the autonomous platform to be the main driver of Tesla’s growth in the coming years, this event could be the most important company one to date.

The valuation remains above peers:

Tesla has been seen as the clear leader in the EV space for some time, and thus it has gotten a very premium valuation. Without adjusting for analyst bottom-line numbers changing in the coming weeks, shares right now are going for about 90 times this year’s expected earnings and more than 50 times if we go out to 2026. Traditional automakers go for earnings multiples in the mid to high single digits at best.

In the chart below, I’ve compared Tesla to a number of EV peers on price to sales, since most of them don’t have any earnings. While Tesla goes for more than 5 times expected 2026 revenues, the average of Lucid (LCID), VinFast (VFS), Rivian (RIVN), XPeng (XPEV), BYD (OTCPK:BYDDF), NIO (NIO), and Polestar (PSNY) actually stands at just over 0.9 times. If we look at more traditional automakers, the price to sales figures drop even further to about 0.3 times.

2026 Price to Sales (Seeking Alpha)

Wall Street will also have some catching up to do in the near term. Going into Tuesday’s report, the average price target on the street was $183, which now implies almost 20% downside from current levels. While I’m sure we’ll see some target hikes in the coming days, this puts Tesla shares the most above the average valuation (in dollar terms) in about 11 months.

Final thoughts/recommendation:

Tesla announced very strong delivery numbers for Q2 on Tuesday, continuing the major rally we’ve seen recently. Despite still reporting a year-over-year decline in unit sales, the print was better than analysts expected and well above some of the worst fears among whisper numbers. The company also showed dramatic growth in energy products deployed, which should help bottom-line estimates turn higher in the coming weeks.

For now, I am keeping my hold rating on the stock. These Q2 numbers were definitely good, but the 40% rally recently gives me a little pause in the short term. Analyst estimates should start to rise, but I’m not sure how much of this beat is now already baked into the stock. I need to see full results first, along with the robo-taxi event, before I can truly buy in, especially at a valuation that trumps every other name in the space.