")

Scott Olson

For many weeks if not months, enough analysts (me included) had been calling for a nearly inevitable recession ahead. The causes and consequences seemed clear: stubborn inflation, rapidly rising interest rates, and the end of the COVID-19 recovery period seemed to be weighing on a few key metrics of economic prosperity, including rising consumer debt service payments relative to income (slightly above pre-pandemic levels, in fact), tanking consumer confidence levels (which, granted, has recovered a bit lately), and a cooling job market, especially in the more cyclical sectors.

Now, fewer of us are so certain that a recession, at least in the US, is imminent. The market seems to have taken note, and the S&P 500 (SPY), whose moves tend to anticipate the economic cycles by several months, has already rallied by 8% so far in 2024 and 32% in the past year.

Below, I explain how leaning into stock market optimism might make sense today, despite fears of rising valuations and the risk of a potential correction ahead. I propose a few trade ideas using the ProShares Ultra S&P500 (NYSEARCA:SSO) as the main holding.

What is SSO?

To get some important basics out of the way, the ProShares Ultra S&P500 is simply a 2x leveraged bet on the broad US stock market index. SSO obtains its leverage exposure by blending a traditional stock portfolio that mimics the S&P 500 with long positions in (1) S&P 500 index swaps and (2) E-mini futures contracts. See SSO’s allocation chart below, by notional value. Keep in mind that the fund’s net assets add up to roughly $4.5 billion.

DM Martins Research, data from ProShares

When it comes to risk and return, SSO simply offers twice the return potential of the S&P 500, minus 91 bps in annual fees and the eventual volatility drag for holding periods longer than a day, while imposing about twice the risk associated with investing in US stocks.

It is very important to point out that SSO’s goal is to produce twice the daily returns on the S&P 500. There is no guarantee that over the longer term (we are talking virtually anything that exceeds a one-day holding period), SSO will gain twice as much as the stock index. For this reason, parking money in SSO and forgetting about it for more than one or a few trading days can be quite dangerous.

The case for investing in the S&P 500

To be bullish on SSO, one must be bullish on the S&P 500 itself since one is a derivative of the other. Because I (1) focus on long-term growth over at least five years, (2) believe in being long beta-positive assets over time, and (3) care little about precisely timing my entries, I am generally bullish on the S&P 500 as a baseline.

That said, and for the reasons discussed above, owning SSO or any other leveraged instrument requires extra caution, including more of a short-term view on the trade timing and the use of risk mitigation tactics (e.g., hedges or stop losses).

So, to start, is now a particularly good time to buy into the S&P 500, after the index gained more than 30% in market value in the past 12 months? The answer is yes, in my opinion.

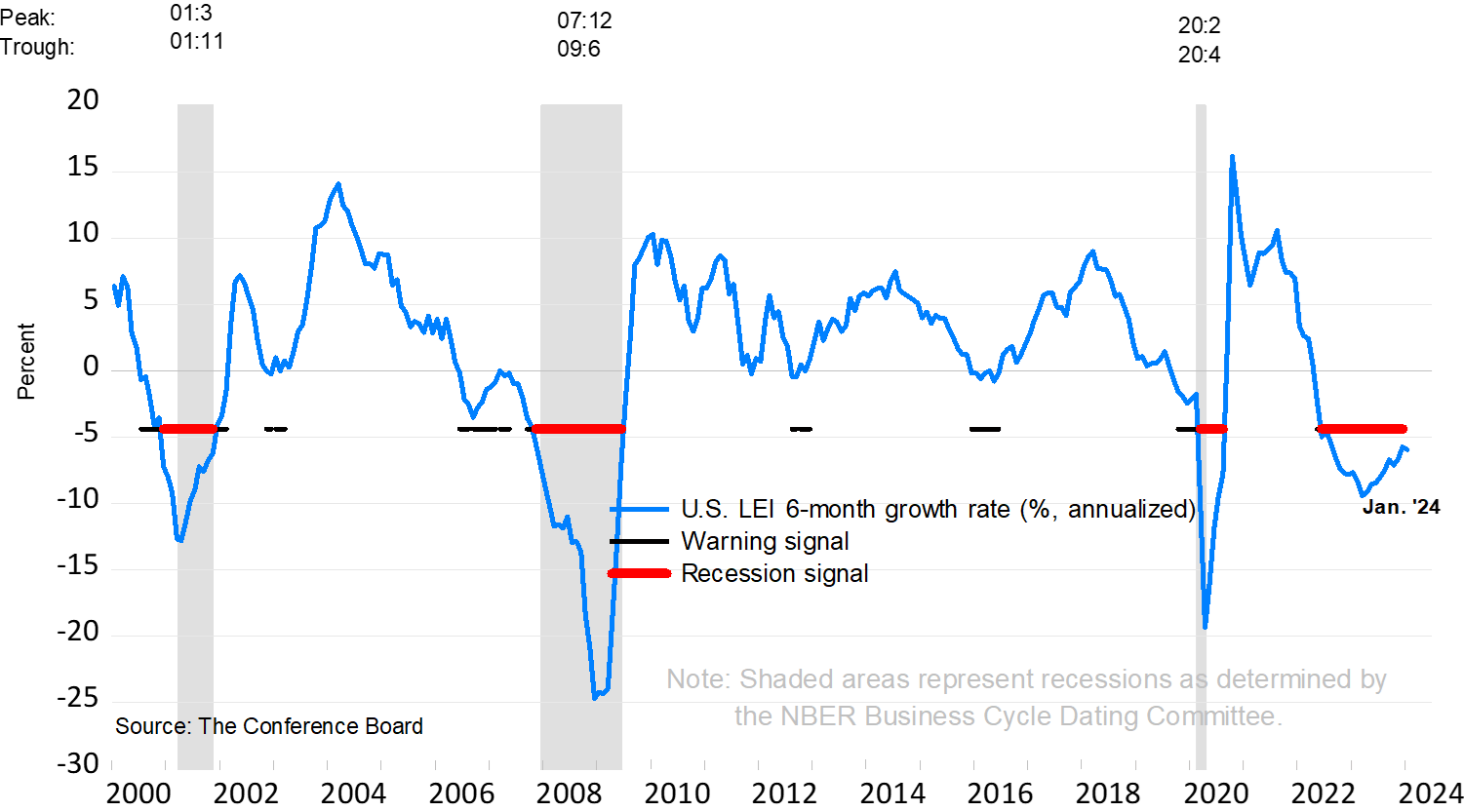

Stocks tend to perform worse during the very late stages of an expansionary cycle or very early stages of economic contraction. The good news is that the leading indicator index depicted below shows that the US economy may end up dodging what, until recently, seemed to be the high likelihood of a recession in the foreseeable future. If confirmed, this would be the first time in about 25 years that a recession signal flashed by the leading economic index would not precede an actual recession.

The Conference Board

In its most recent report, the Conference Board summarized the current landscape as follows:

While the declining LEI continues to signal headwinds to economic activity, for the first time in the past two years, six out of its ten components were positive contributors over the past six-month period (ending in January 2024). As a result, the leading index currently does not signal recession ahead. While no longer forecasting a recession in 2024, we do expect real GDP growth to slow to near zero percent over Q2 and Q3.

To emphasize, the economy is not on its strongest footing, necessarily. Manufacturing new orders are still soft. Consumers remain skeptical of business conditions. The yield curve is still sharply inverted between the 3-month and 10-year maturities (5.5% vs. 4.3%, respectively). Average weekly manufacturing hours, at 39.9, are still near the lowest since 2010, excluding the early COVID-19 period. Plateauing inflation numbers are likely to delay the Federal Reserve’s move to lower interest rates in 2024.

The important point, however, is that the economy does not seem to be in as bad a shape as it was a mere six months ago. In my view, being out of the S&P 500 would require more than a few weak spots in economic indicators and valuations that, while rich today, are probably not at unreasonable levels.

How to introduce SSO in the portfolio

Contrary to popular belief, the riskiest time to own a risky asset like the S&P 500 (let alone a leveraged fund based on it, like SSO) is when the index is in a severe drawdown, and not when it is hovering around all-time highs.

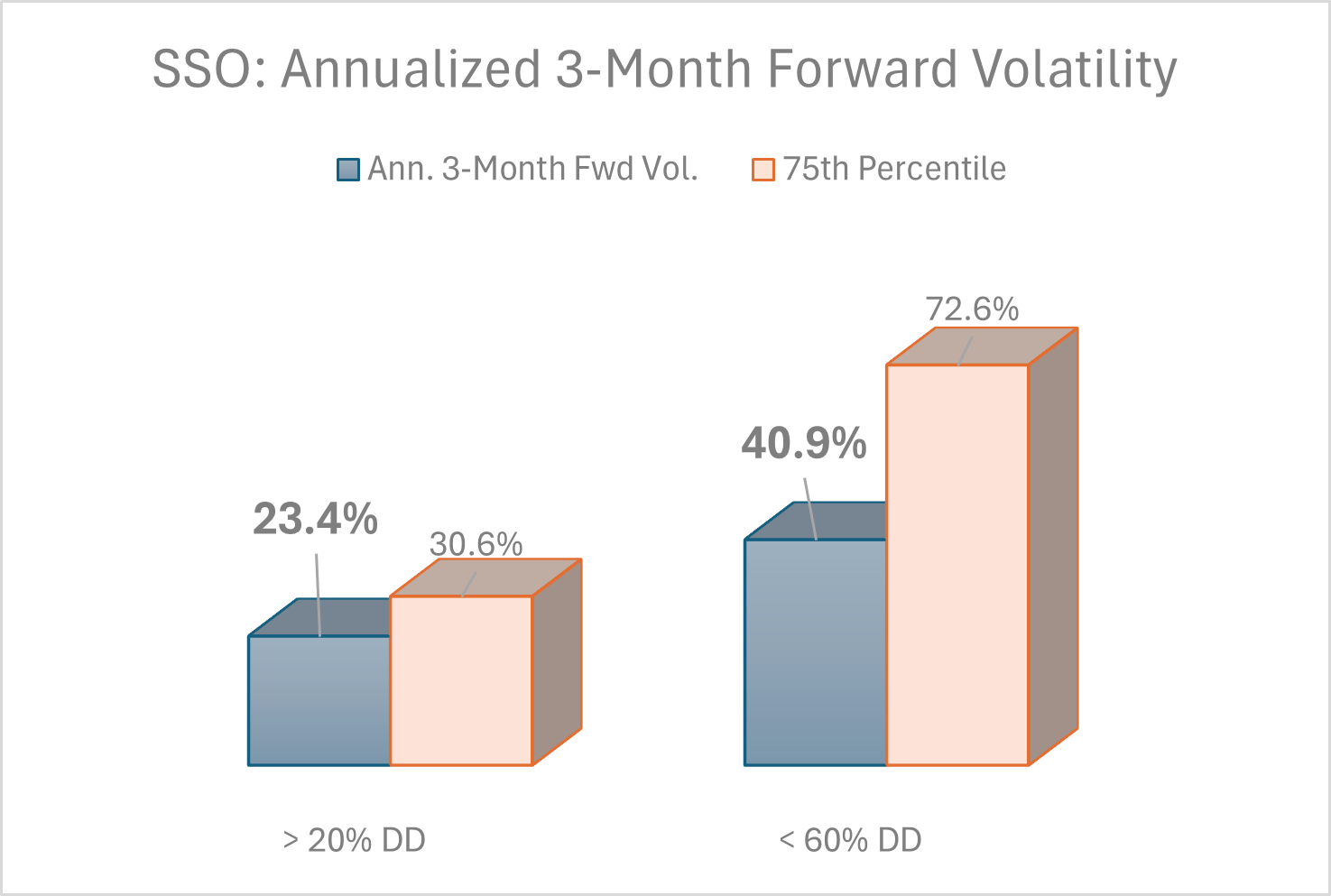

The chart below shows that the three-month forward, one standard deviation (a measure of volatility) of the average daily return produced by SSO was much higher (i.e. more jittery and, therefore, more unpredictable) when the fund was in a 60%-plus drawdown: nearly 41%. At the 75th percentile, volatility was a whopping 73%.

DM Martins Research, data from Yahoo Finance

Conversely, owning SSO when the fund was in a drawdown of 20% or less (i.e. when the S&P 500 was not in correction territory, which is the case today) produced much lower volatility of 23%. At the 75th percentile, the volatility was still a fairly tame 31%, considering a leveraged fund that is otherwise regarded as very risky.

Therefore, at least judging by historical performance, SSO may be a less risky holding today than it would be if the S&P 500 were in trouble. While this setup does not make SSO a safe investment in any way, it may help to reduce the potential risk of high volatility or sizable losses in the next three months.

Even so, I think that SSO should be used cautiously. The following would be three approaches to adding SSO to a growth portfolio.

- Simply overlay a small amount of SSO on a core S&P 500 position (say, 10 parts SSO for 90 parts SPY) for as long as the stock index is trading within 5% to 10% of all-time highs. While SPY is making fresh highs, the SSO position would likely continue to boost the portfolio’s returns. Once the S&P 500 begins to correct, but early enough in the process, sell SSO and stop the losses.

- Combine ProShares Ultra S&P500 with a hedging instrument, as I proposed in 2021. SSO plus a long VIX fund (VIXY), at a ratio of about 90/10 or 92/8, could help to soften the blow in case the S&P 500 falls off the cliff suddenly. One could diversify the hedge further by introducing an anti-beta fund (BTAL) to the position.

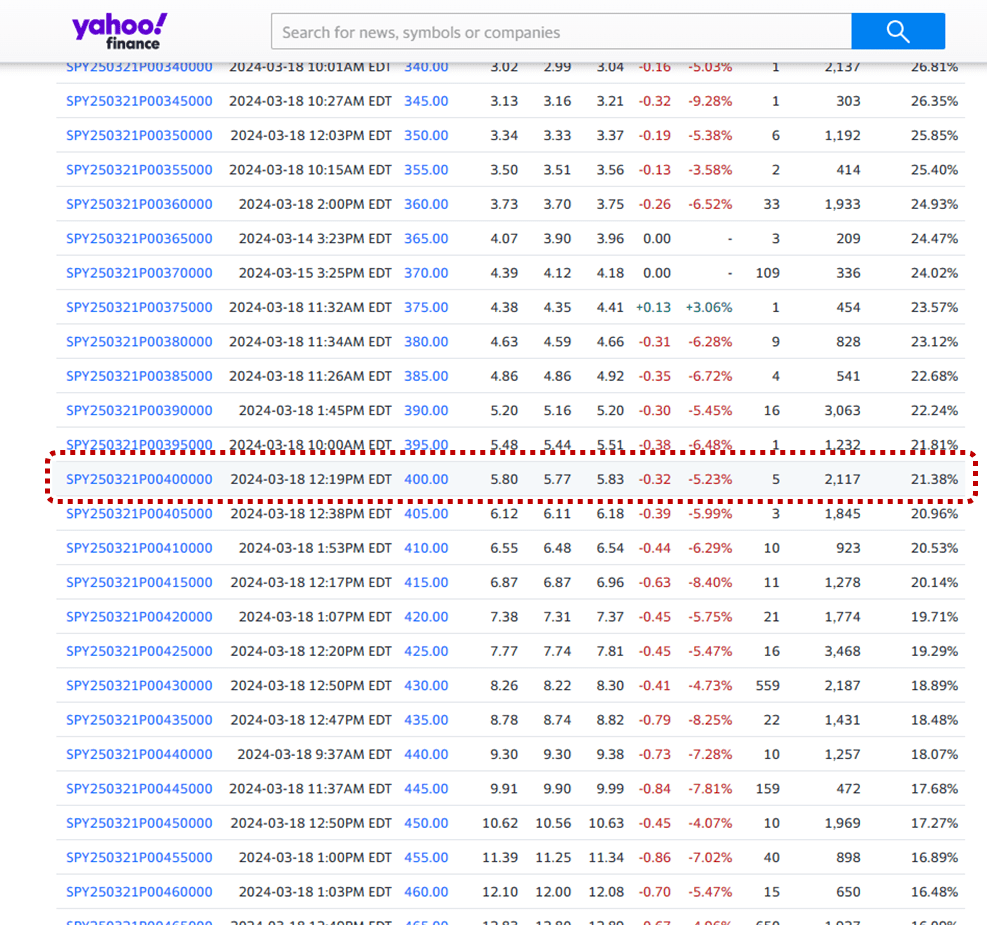

- Lastly, hold SSO alongside an out-of-the-money put on the S&P 500, taking advantage of today’s low volatility environment that helps to keep option prices low. For example, as depicted below, $5.80 in option premium buys a $400 SPY put expiring in one year, which limits the downside on an S&P 500 position to 22% (or, roughly speaking, 44% on SSO, in addition to the volatility drag). The 1.1% “cost” of hedging away fat tail risk seems reasonable in exchange for the outsized potential upside from owning the Ultra S&P 500 fund.

Yahoo Finance