Kent Nishimura/Getty Images News

It seems pretty clear at this point that the path for monetary policy is higher for longer. Odds for rate cuts have reduced from an unthinkable 7 in January to just 1, with decent odds for 2. Listening to Fed speakers since the last FOMC rate decisions. They seem to be saying the same thing; given the lack of confidence in a disinflationary trend that started late last year, many members now say it will take longer to see cuts. Some even question whether the neutral rate is higher today or if the policy is restrictive enough.

Don’t be surprised if the April CPI report suggests more trouble for the Fed. At this point, it seems clear that the CPI is not on a pace to get 2 percent anytime soon. It has been rising at a roughly 3.5% pace since the summer of 2022.

The April CPI report will continue along with that 2022 trend and is forecast to show that the previous three months of hot prints were no fluke, and April could be even worse, even if it comes in as expected. For April, CPI is expected to increase by 0.4% m/m versus last month’s 0.4% while rising by 3.4% versus last month’s 3.5%. Core CPI is expected to cool to 0.3% versus 0.4% while increasing by 3.6% y/y, down from 3.8%.

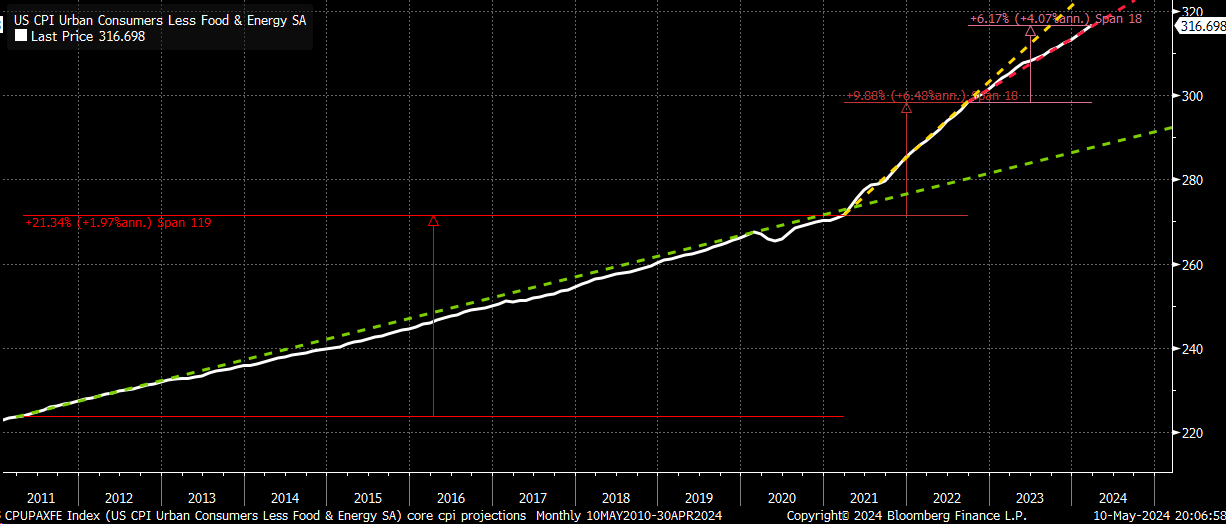

On 3.5% to 4% Run Rate

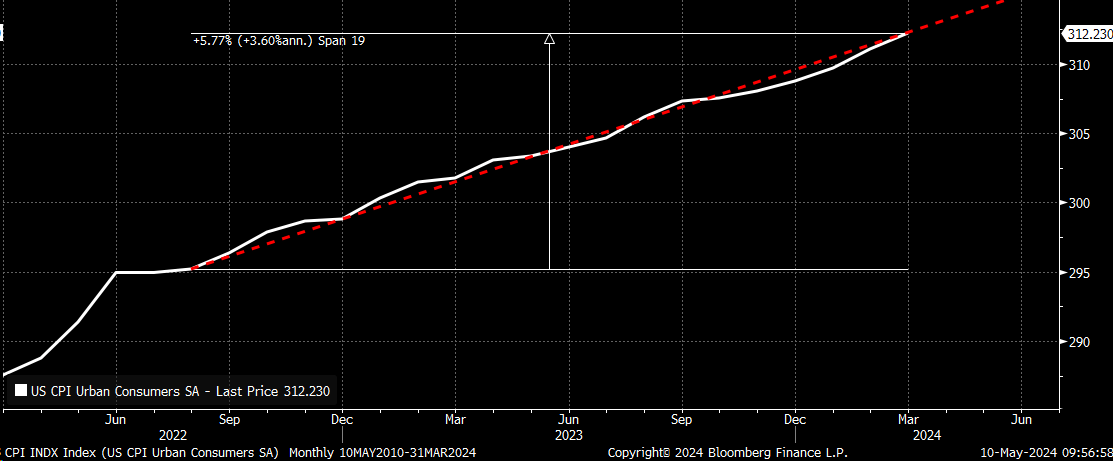

The CPI, after all, is just an index of goods and services, and the index, both seasonally and non-seasonally adjusted, has been rising consistently since August 2022 in a nearly linear path. The biggest problem is that the path doesn’t appear to be derailing either; it just continues to move higher with very few deviations. Since August 2022, the CPI seasonally adjusted has risen linearly at an annualized growth rate of 3.6%. This trend has been in place for 19 months at this point.

Bloomberg

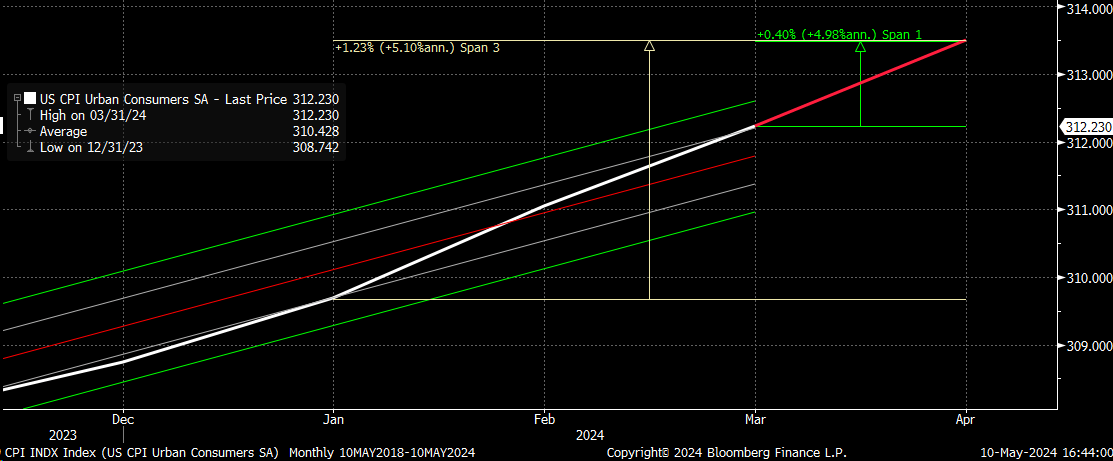

But if analysts are correct, and the CPI rises by 0.4% m/m, then it is possible that the trend is changing, and to a path faster than the previous trend. This would put the CPI on a path for annualized growth of 5.1% over the past three months, seasonally adjusted.

Bloomberg

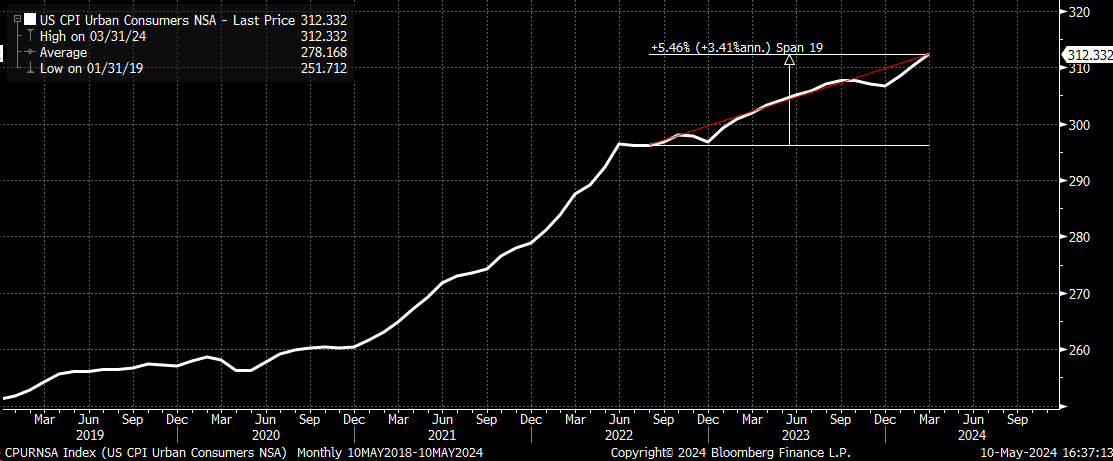

Additionally, the non-seasonally adjusted index measures the y/y rate of change in the actual CPI headline report. This measure shows that since August 2022, the CPI has risen at an annualized growth rate of 3.4%. Another 3.4% y/y increase in April would be another at-trend month for the CPI NSA.

Bloomberg

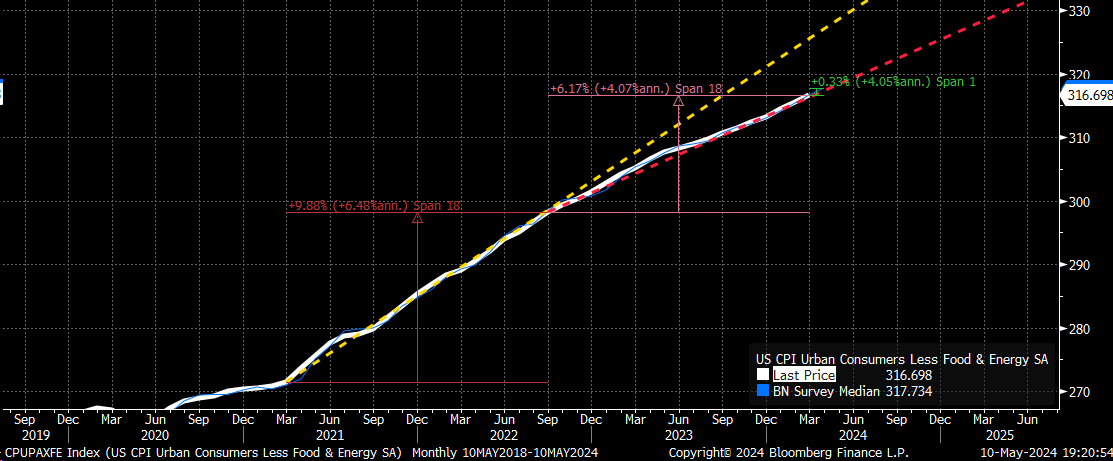

Even core CPI has been around a 4% growth rate since September 2022. If the core CPI comes in as expected in April at 0.3% m/m, the core CPI will still be running at the trend that started 19 months ago. It is hard to look at this data to see where the disinflation process occurs. To this point, since March 2021, the disinflation process has shifted to a lower pace just one time. Perhaps a lower gear is coming again soon, but at least based on estimates, that isn’t likely to happen in April.

Bloomberg

The current rate of change for the core CPI is nowhere close to the 2% growth rate seen over the 119 months between 2011 and the middle of 2021. It clearly shows that the growth rate in the core CPI is rising at a rate that is faster than what is required to achieve that 2% growth rate, and it would require additional slowing to get there; the core CPI is not currently on that path.

Bloomberg

Hotter Headline CPI

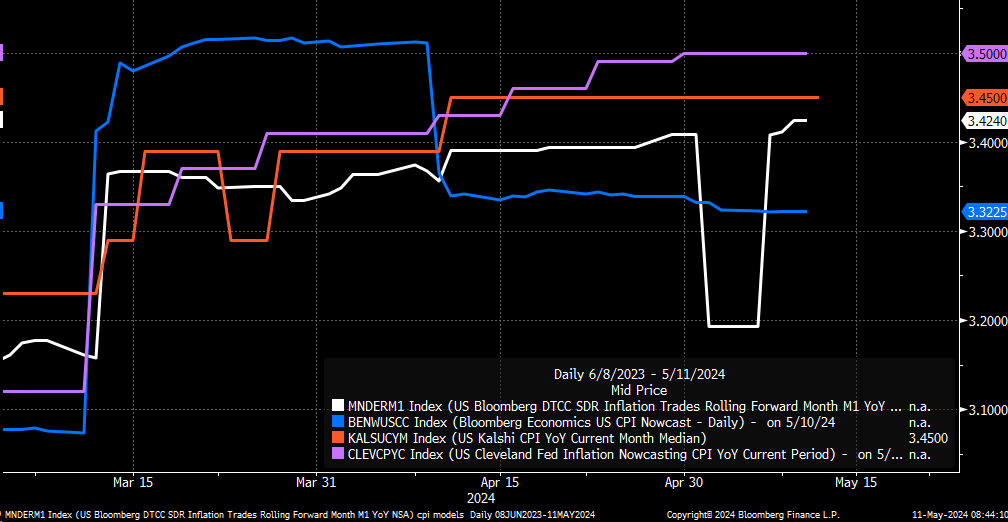

CPI swaps are assigning a risk of the CPI report rising by more than 3.4%, with swaps currently trading at 3.42%. Meanwhile, Kalshi is pricing in a CPI of 3.45%, the Cleveland Fed is pricing at 3.5%, and Bloomberg Economics is pricing at 3.32%. That gives us three out of four inflation models estimating the potential for CPI rising faster than the annual analysts’ forecast of 3.4% on a year-over-year, non-seasonally adjusted basis.

Bloomberg

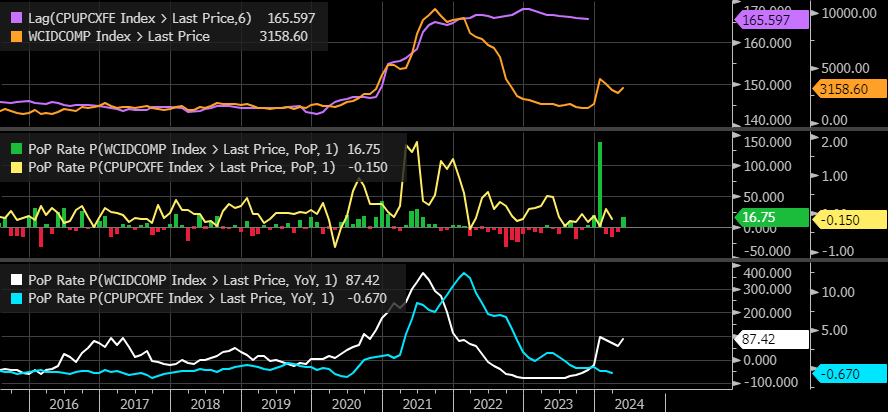

Given some of the data we have seen thus far, it would not be surprising to see a hotter-than-expected CPI report in April, as the models and swaps are projecting. Shipping rates have surged since the start of the year, and to this point, we haven’t seen a surge in goods prices yet. The CPI Commodities Excluding Food and Energy Commodities Index tends to track changes in the WCI Container Freight Rate by around six months. If the “goods” pricing index starts to reflect higher shipping prices, then that sixth month is coming soon.

Bloomberg

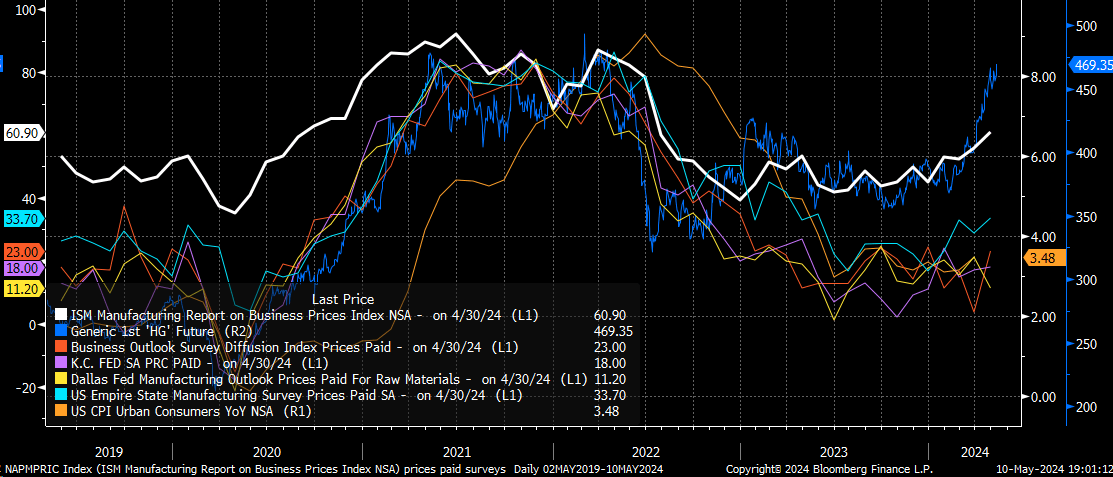

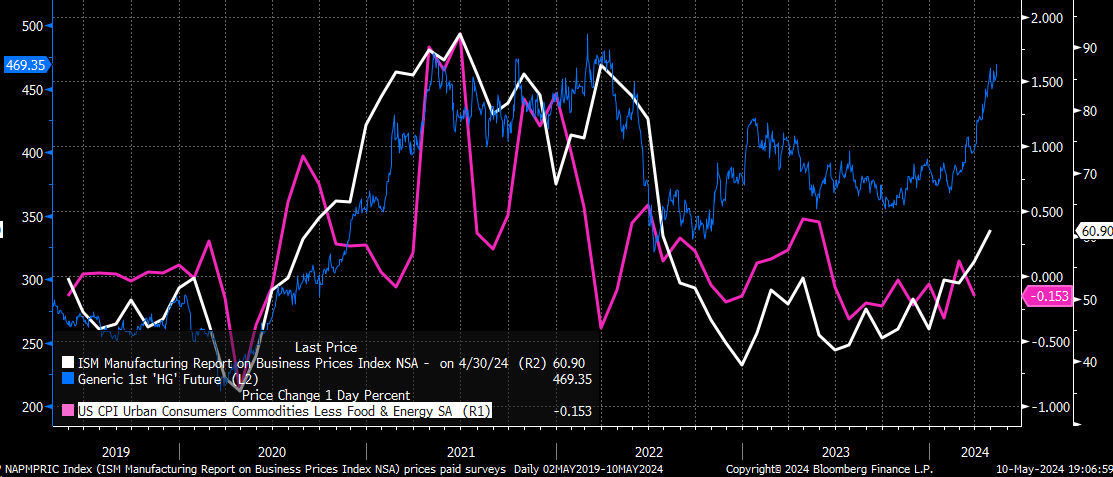

Also, the ISM manufacturing prices paid increased in April by its fastest since the summer of 2022. Many regional Fed surveys, such as the Philadelphia Fed, Empire State, and KC Fed, also show higher prices in April. The Dallas Fed was the only region that saw a downturn in April.

Bloomberg

The trends for higher prices in some of these regional surveys and commodity prices could again show up in goods prices in April. This is something of note because, generally speaking, energy and goods disinflation and even deflation have helped offset much of the gains we continue to have in services inflation.

Bloomberg

Even if the numbers do not surprise the upside, it won’t be a win for the Fed. CPI numbers are running too hot at this point; the trends are running the wrong way. Instead of heading toward 2% inflation, it is running at 3.5% and potentially at risk of running even hotter.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.